Weekly Market Movers | July 6, 2026

10 minutes

This week on Weekly Market Movers, Doug covers the following:

- Markets gained overall, led by large U.S. stocks, while small caps lagged.

- Economic data sent mixed signals, with softer hiring but stronger consumer confidence and job openings — which continued to point to a growing economy.

- Inflation and interest rates remained top concerns by investors, with most expecting rates to stay higher for longer.

- The Fed stayed in focus as investors watched for clues on future rate hikes and inflation policy.

- Geopolitical tensions — primarily in the Middle East — continued to create uncertainty, though oil prices remained relatively stable.

- Questions about whether heavy AI spending will pay off weighed on chip and technology stocks, including semiconductor companies in South Korea.

- Credit markets remained resilient, signaling confidence in corporate earnings and balance sheets.

- International markets outperformed, while emerging markets were mixed due to renewed concerns around AI spending.

- Earnings season is getting underway, with investors looking for proof that companies can deliver the strong growth expectations currently priced into markets.

Watch the full video:

Chart of the Week:

TRANSCRIPT:

Hello everyone, and welcome to the Weekly Market Movers series presented by Wealth Enhancement. My name is Doug Huber. I’m the Deputy Chief Investment Officer, and today we’re going to cover some of the topics we saw last week during the shortened Independence Day holiday week.

We had a few economic releases that we want to cover. This included a slightly disappointing employment report for June. However, we did see improvements in consumer confidence and job openings, and while there was a small drop in the ISM manufacturing numbers, the index remains in expansionary territory.

Equities were mixed for the week. We saw net gains in U.S. and developed markets, while tech-oriented parts of emerging markets experienced some weakness, and we’ll touch on that shortly.

Bonds were mixed as well, with yields rising in response to continued inflation concerns. Commodities saw minimal movement in energy but more volatility elsewhere. We’ll get into all of that as we go through today’s update.

On the economic side, the ISM Manufacturing Report, which is a good indicator of economic activity, declined by 0.7 points to 53.3. That was below the consensus estimate of 53.9. However, at the end of the day, it still indicates an expansionary pace, meaning the economy continues to grow. If you look through the report and read some of the commentary, many respondents described core business activity as remaining solid despite ongoing geopolitical concerns.

Those are positive signs that the economy continues to expand.

We also saw the JOLTS, or Job Openings and Labor Turnover Survey, report for May. Job openings increased to 7.594 million, above the forecast of 7.296 million. That indicates employers are hiring, which is a positive development.

Overall, the JOLTS level has moved back toward the higher end of the range we’ve seen over the last two years. We do think some of that may have been driven by hiring ahead of World Cup-related activity, which tends to generate seasonal or temporary hiring needs. Regardless, it was a strong number.

On the flip side, jobless claims fell to 215,000, below the estimate of 218,000. Again, that’s encouraging. We’re not seeing significant layoffs or firings, which is a positive sign.

However, the Employment Situation Report, including the nonfarm payrolls numbers, came in a little softer. That included downward revisions to both April and May, along with some weakness in June’s data.

Looking beneath the surface, we saw gains in professional services, social assistance, and healthcare. However, leisure and hospitality employment declined by about 61,000 jobs. I think that reflects some of what we discussed earlier. Hiring activity may have increased in anticipation of World Cup-related events, and now some of that earlier hiring is beginning to normalize.

Turning to the markets, it was a strong week for equities. The S\&P 500 gained approximately 1.78% for the week, while the tech-heavy Nasdaq rose 2.12%. Small-cap stocks experienced some weakness, declining by about 42 basis points.

If we dig a little deeper, market performance reflected mixed economic and employment data, but large-cap growth stocks outperformed while small caps lagged somewhat. On the sector side, communication services, financials, consumer discretionary, and healthcare were among the strongest performers. Energy and utilities were the weakest sectors, each down roughly 1% for the week.

The biggest decline occurred in technology during the final few days of the week due to concerns surrounding the pace and scale of AI-related infrastructure investments.

On the geopolitical front, the memorandum of understanding between the U.S. and Iran remains in place. However, periodic skirmishes continue, which has added some volatility to markets. Even so, investors largely appear focused on economic expansion and earnings growth prospects, and we’ll discuss that further in a moment.

We also saw the U.S. Supreme Court rule against the administration, allowing Fed Governor Lisa Cook to remain on the Federal Reserve Board. Markets viewed this as reinforcing the independence of the Federal Reserve. That independence is important to financial markets, and the ruling signaled that the Fed continues to be treated differently from other federal agencies where leadership changes have been more common.

International stocks were generally positive, particularly in Europe and Japan. Developed markets benefited from a somewhat weaker dollar in the Eurozone and a degree of normalization in the Middle East.

The Japanese yen, however, continues to trade near its weakest level in approximately 40 years. Part of that reflects Japan’s desire to maintain a weaker currency to support exporters, but the country also faces elevated debt levels. We’ll continue monitoring that situation closely.

Emerging markets were mixed. Taiwan and China posted gains, but those were offset by declines in Brazil and, more importantly, South Korea. South Korea represents a significant portion of the emerging markets index and is heavily weighted toward Samsung and SK Hynix, two major semiconductor companies.

Late in the week, both companies experienced notable declines due to concerns about potential overinvestment in AI infrastructure.

Some of those concerns were fueled by comments from Meta indicating it may attempt to sell some of its computing capacity. There will likely continue to be debate about the appropriate level of AI-related investment. Historically, new technologies often experience periods of overbuilding. However, that excess capacity is typically absorbed over time. It will be an important theme to watch in the months ahead.

As I mentioned earlier, bonds delivered mixed results. U.S. Treasuries and investment-grade bonds declined as yields moved higher. However, the riskier segments of the credit markets, including high-yield bonds and floating-rate bank loans, posted positive returns. That suggests investors continue to see a healthy corporate backdrop and remain confident in companies’ ability to service their debt obligations.

Another factor affecting bond yields was commentary during the ECB Central Bank Forum in Portugal. Fed Chair Kevin Morris continued to emphasize that inflation remains too high. As a result, markets appear to be maintaining expectations for a higher-for-longer interest rate environment and, potentially, additional rate hikes.

Looking ahead to the coming week, interest rates will remain a key focus. The Federal Open Market Committee, or FOMC, will release its meeting minutes, providing additional insight into policymakers’ thinking. We will also see auctions for three-year, ten-year, and thirty-year Treasury securities, and we’ll be watching to see whether increased supply has any impact on rates.

I do think the FOMC minutes may reveal growing concern about inflation. However, if commodity prices continue to normalize as tensions in the Middle East ease, that should eventually help moderate inflation pressures. Markets would likely respond positively to that development.

Another key item to watch is the beginning of second-quarter earnings season. While we are now in the early stages of the third quarter, companies will begin reporting second-quarter results.

It is a relatively light week for earnings, with major bank earnings still a couple of weeks away. However, companies including Levi Strauss, PepsiCo, WD-40, and Delta Air Lines are scheduled to report. Their results should provide valuable insight into consumer demand, travel trends, freight activity, and margin pressures.

Markets pay close attention to these early reports because investors often use them to gauge broader trends and estimate how upcoming earnings releases may unfold across other industries.

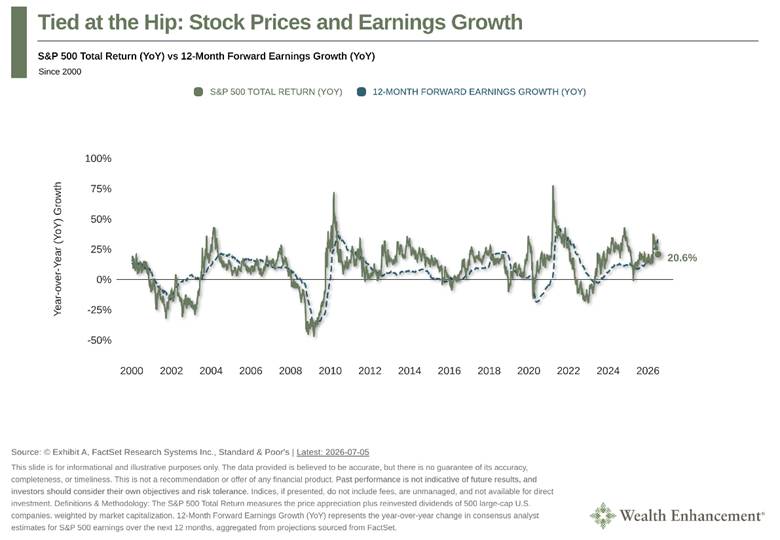

There is one chart I would particularly like to highlight because I think it illustrates a key driver of market performance.

Stock prices are closely tied to future earnings growth. Ultimately, investors are paying for the potential growth of a company’s future earnings. In this chart, the dotted blue line represents twelve-month forward earnings growth, while the other line reflects total returns for the S\&P 500. The relationship between the two is remarkably strong.

Over the trailing twelve months, the S\&P 500 has returned approximately 20.6%. Interestingly, expected earnings growth over the next twelve months is approaching 30%.

That outlook supports the case for continued economic expansion and potentially higher stock prices. However, these are still forecasts. As we move through earnings season, execution matters. Investors will be focused not only on reported results but also on the guidance companies provide for the future.

It should be an exciting earnings season, and we’re eager to see what the data reveals. The earnings reports ahead will help determine whether the economic expansion reflected in recent data is translating into real business performance.

We look forward to following up with you next week, and thank you for tuning in to the Weekly Market Movers video series.

This information is not intended as a recommendation. The opinions are subject to change at any time and no forecasts can be guaranteed. Investment decisions should always be made based on an investor’s specific circumstances. Investing involves risk, including possible loss of principal.

2026-13067

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.