Weekly Market Movers | June 29, 2026

7 minutes

This week on Weekly Market Movers, Gary covers the following:

- Concerns about high AI stock prices added volatility, starting in global chip stocks and spreading to U.S. markets.

- Investors shifted from tech into more stable sectors like healthcare and real estate.

- AI demand remains strong, but questions are growing about whether spending will pay off.

- Interest rate expectations moved higher, with rates likely to stay elevated.

- Bond markets became more volatile amid uncertainty around inflation and the Fed.

- Oil fell toward $70, easing inflation pressure—but risks remain.

- Middle East tensions continue to add uncertainty to energy prices and inflation.

- Big AI companies still lead, but more stocks—including small caps and international—are starting to participate.

- With uncertainty still elevated, staying diversified remains key.

Watch the full video here:

Chart of the Week

TRANSCRIPT

Hi, I’m Gary Quinzel with Wealth Enhancement. Welcome to the Weekly Market Movers. Let’s take a look at what drove the markets last week.

The most significant driver was the sharp reassessment of AI-linked valuations triggered by what happened in the South Korean market.

As you may know, South Korea produces the vast majority of semiconductors on the planet. Two companies in particular, SK Hynix and Samsung, each fell by more than 10%, which triggered rising concerns. It actually cascaded into the U.S. market as we saw the Philadelphia Semiconductor Index also fall considerably, roughly 5% on Friday alone. All of that led to continued concerns around AI-linked valuations, how expensive these companies have become, how concentrated these companies have become, and the vast amount of performance that has been attributable to them.

Of course, we know that can work in both directions, and so we saw volatility after Micron reported. Even though it was considered a stellar report and beat guidance, we still saw continued volatility around what’s going on there, what’s going on with OpenAI’s IPO, and all of that tech weakness led to a classic rotation into more defensive sectors, things like healthcare and REITs.

Even within the S&P 500, if we take a look at the equal-weighted version of the index as opposed to the market-cap-weighted version that we typically focus on, the equal weight is now at all-time highs, even though we saw some of those bigger market-cap names struggle a little bit. That was the main driver, and we saw a little bit of weakness across the board. But overall, equity markets are hanging in there for a pretty strong quarter as we look to turn the page into the third quarter.

There still remain a lot of questions and concerns, particularly around inflation and what the next move will be by new Fed Chair Kevin Warsh.

If we look at what the futures market is pricing in, investors are now expecting a greater possibility of rate hikes as opposed to rate cuts. Even strategists at Bank of America have talked about potentially as many as three rate hikes this year. Minneapolis Fed President Neel Kashkari has also talked about rate hikes. All of that is triggering more concerns around a higher-for-longer interest rate environment, which is causing volatility across the fixed-income landscape. There’s simply more uncertainty around where rates will be headed next.

On the positive side, oil is certainly heading lower. We saw Brent crude retreat to around $70 a barrel, which was certainly a sigh of relief, particularly for those in Europe, but generally for everyone involved who fills their gas tank or relies upon energy as a source for their business. It’s certainly welcome relief, and as we continue to get more optimistic news coming out of the Middle East and optimism around a more permanent ceasefire involving the U.S., Iran, Israel, and Hezbollah, that could continue to push prices a little lower. Fingers crossed that we’ll continue to see that trend.

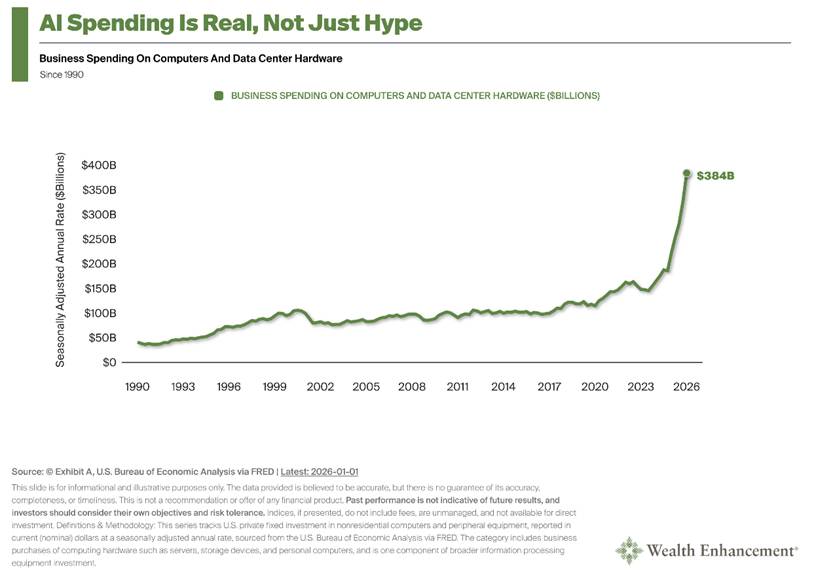

With that, I’m going to share a chart here that I thought was quite interesting. This is our Chart of the Week, and it’s about AI spending.

There’s a lot to take away from this chart, but the most notable trend is how much growth in investments in computers and computer equipment has changed since 1990, when this data series begins. The data comes from the U.S. Bureau of Economic Analysis, or BEA, and feeds directly into GDP calculations.

What we can see is that from 1990 through around 2023, when ChatGPT first hit the mainstream, year-over-year growth averaged roughly 4% annualized. Then we hit 2023, and it went parabolic. We’ve now seen that year-over-year growth, albeit for only about two and a half years, skyrocket to roughly 50%.

So what exactly is driving that growth? It’s fairly obvious. Massive spending on the infrastructure needed to support the AI buildout. A huge portion of that spending is related to the hyperscalers, the major providers of cloud services such as Microsoft, Amazon, and Google.

Hyperscalers are pulling forward infrastructure spending due to exceptionally strong demand. In fact, Microsoft recently indicated that customers cannot deploy AI capacity fast enough.

As a result, investment dollars are flowing into every part of the physical AI layer. That’s GPU servers, custom chips, networking equipment, storage, cooling systems, power equipment, and the data center capacity needed to support it all.

It’s even showing up in the results of companies supplying that infrastructure. Nvidia, for example, reported fiscal 2027 first-quarter data center revenue of approximately $75 billion, up about 92% year over year. That’s substantial growth.

Of course, the risk is that the capital expenditures come before the payoff. The return on investment may not ultimately justify the spending, and we’ll have to see how that develops. But for now, what we do know is that there is massive spending taking place, and that is helping fuel earnings growth. It’s helping fuel the AI tailwind that continues to support the market.

Other than that, as the second quarter comes to an end, it has been quite strong. We have seen broader growth from various participants across the equity landscape. We’re seeing stronger growth out of emerging markets, better growth internationally, and increased participation from Russell 2000 small-cap stocks.

That leads us to believe that overall, the market and the economy are on relatively solid footing. But as always, we do have our concerns. That’s why we maintain diversified portfolios, and why we advise our clients to stay diversified and be prepared for a broader range of potential outcomes.

That’s it for this week. We’ll talk to you soon. Take care.

This information is not intended as a recommendation. The opinions are subject to change at any time and no forecasts can be guaranteed. Investment decisions should always be made based on an investor’s specific circumstances. Investing involves risk, including possible loss of principal.

2026-13015

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.