Retirement Readiness: 5 Steps to Get Ready For Retirement

4 minutes

Retirement planning can feel like navigating a sailboat through the Bermuda Triangle. From shifting inflation rates to unknowable health care costs, it can seem impossible to know exactly what route to take and how much to save. That’s why we created a Retirement Income Calculator to help you estimate what you may need to save to support your lifestyle into retirement.

What Is Retirement Readiness?

Retirement readiness means having a financial plan in place that helps support your desired lifestyle after you stop working. It includes understanding your retirement savings, future retirement expenses, Social Security timing, health care costs in retirement, taxes, and retirement income strategy so you can answer an important question: “Am I ready to retire?”

Key Takeaways

- Retirement readiness involves more than hitting a certain age—it means creating a sustainable retirement income strategy.

- Understanding your retirement expenses, taxes, and health care costs can help you estimate how much income you may need in retirement.

- Your target retirement age and Social Security claiming strategy can significantly impact your retirement income.

- Inflation, withdrawal strategy, and investment allocation all play a role in long-term retirement success.

- Using a retirement readiness checklist and retirement income calculator can help identify potential retirement income gaps before you retire.

Are you financially prepared for retirement?

According to the 23rd Annual Transamerica Retirement Survey of Workers, a third of American workers are not confident that they will be able to fully retire with a comfortable lifestyle.

Generation X is the least confident generation by far. A staggering 40% of Gen X survey respondents stated that they are not confident they will be able to retire comfortably. Meanwhile, a full 30% of Millennials and Baby Boomers responded that they are not confident. Gen Z came in as the most confident, with only 26% of Gen Z survey respondents stating they are not confident.

While retirement confidence levels can fluctuate over time depending on market conditions, inflation, and economic uncertainty, the survey highlights an important reality: many Americans still wonder how much they need to retire comfortably and whether they’re truly prepared.

If you happen to be among the large group of people who aren’t confident in their ability to retire comfortably, there are steps you can take to course-correct.

By following along through these next sections and considering the questions as they apply to your unique situation, you’ll set yourself up to use our retirement income calculator to your best advantage.

Check your retirement readiness with our Retirement Income Calculator

Retirement Readiness Checklist

Before diving into the five steps below, use this retirement readiness checklist to evaluate whether you may be on track.

Timeline | What to Review | Why It Matters |

10+ years before retirement | Retirement savings rate, investment allocation, debt reduction, equity compensation, business succession planning | Helps maximize compound interest and long-term growth |

5 years before retirement | Retirement income projections, Medicare and retirement planning, tax planning before retirement, withdrawal strategy | Helps identify potential retirement income gaps |

1 year before retirement | Social Security claiming strategy, estate planning, beneficiary reviews, health care costs in retirement | Prepares your transition into retirement |

Year of retirement | Retirement withdrawal strategy, portfolio income planning, lifestyle spending, inflation adjustments | Supports sustainable retirement income |

5 Steps to Get Financially Ready for Retirement

Retirement readiness isn’t just about reaching a certain age. It’s about ensuring you have the financial security to enjoy the next phase of your life—whatever that phase might look like. But how can you know that you’re on the right track? It starts with understanding your current financial status and projecting what your future needs might be.

1. Assess your current financial status and retirement income strategy

First of all, you need to figure out how much you have.

Is your nest egg spread across multiple different accounts, like 401(k)s or IRAs? If so, do you understand the different tax implications of those accounts, and how your future tax burden could change the underlying variables of your retirement income strategy?

Tax planning before retirement can play an important role in helping you create a more tax-efficient retirement income strategy. Understanding how taxable, tax-deferred, and tax-free accounts work together may help reduce unnecessary taxes later in retirement.

Alternatively, is much of your net worth tied up in your business? If so, do you have an exit plan in place to turn that illiquid wealth into tangible retirement income?

Retirement planning for business owners often requires additional considerations, such as succession planning, liquidity timing, and how to turn business equity into retirement income. Similarly, high-net-worth individuals and professionals with concentrated stock positions or equity compensation may need additional diversification and risk-management strategies before retirement.

As part of your pre-retirement checklist, you may also want to evaluate outstanding debt, emergency savings, insurance coverage, and estate planning documents.

While you’re looking at your investments and savings, it’s also a good time to consider what your current lifestyle looks like, and how that lifestyle might change after you enter retirement. Are you planning to stay in the same house? Do you have extensive (expensive) travel plans? Are there items on your bucket list that you can’t wait to complete?

It might seem a bit early to do so, but now is the perfect time to start generating a ballpark number to target for your desired retirement income.

2. Estimate your future retirement expenses and health care costs

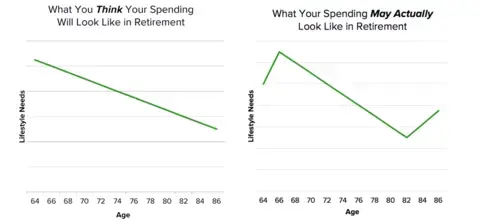

Whether you like it or not, retirement will bring a shift in your expenses. Some costs might go down, like your gasoline bill if you’re a daily commuter. However, other costs might go up, like health care.

At Wealth Enhancement, we often find that our clients’ overall expenses actually increase when they enter retirement. You’re still young and full of energy, so you start scratching items off of your bucket list and don’t slow down for a while. As retirement goes on, you may see those expenses slowly and steadily decrease. However, later in retirement, you might find that your spending actually increases again, as you start needing to shell out more for health care expenses.

Health care costs in retirement are one of the most commonly underestimated expenses. Medicare and retirement planning should include considerations for premiums, supplemental insurance, prescription drug coverage, and potential long-term care costs.

In addition to health care, think about housing, travel, family support, charitable giving, and lifestyle spending when estimating retirement expenses. These factors can all influence how much retirement income you may need.

Don’t let this graph scare you. If you’re here and thinking about your retirement income plan early, then you’re on the right track to having enough money to adequately fund your retirement.

3. Determine your target retirement age and Social Security claiming strategy

Retirement doesn’t just automatically happen when you turn 65. It’s been said before: retirement isn’t an age—it’s a state of financial readiness. The earlier you start saving and planning for retirement, the more time your money has to grow through compound interest.

As you review your current investments and consider how much more you need to save, think about the power of compound interest. Compound interest happens when you earn interest on the money that you’ve already invested, then reinvest that money to keep earning more interest on it. In other words, the longer you keep your money invested, and the more money you save, the more compound interest can work for you.

Our retirement income calculator assumes that your investments will earn a certain percentage of compound interest over time, so you fortunately don’t have to do the math yourself. But do keep in mind that investing earlier may mean that you can potentially choose an earlier target retirement age.

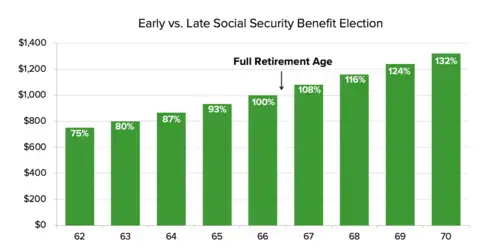

Another consideration when it comes to your expected retirement age is your Social Security claiming strategy. Many people don’t know this, but you can actually apply to start receiving your Social Security benefits as early as age 62. The catch is that you’ll receive a 25% lower benefit for the remainder of your retirement.

Your Full Retirement Age (FRA) depends on the year you were born. For many Americans born in 1960 or later, FRA is age 67. Claiming benefits before FRA reduces your monthly benefit amount, while delaying benefits beyond FRA can increase your payments through delayed retirement credits up to age 70.

Your Social Security strategy is a risk-benefit analysis that’s best done with the experienced guidance of a qualified financial advisor.

4. Factor inflation, taxes, and withdrawal planning into retirement

In 2022 and 2023, we all experienced the searing pain of inflation on our savings, earnings, and expenses. Inflation can erode the purchasing power of what you’ve already saved up. Although it’s difficult to explicitly plan for inflation, diversifying your investment portfolio and regularly reviewing your portfolio allocations can help cope with the threat of future inflation.

Understanding how inflation affects retirement savings is especially important for retirees who may spend decades relying on portfolio income. Retirement withdrawal strategy, tax-efficient income planning, and maintaining diversified investments can all help address inflation in retirement.

It’s also important to consider sequence-of-returns risk, which refers to the impact that poor market performance early in retirement can have on long-term portfolio sustainability.

5. Use a retirement income calculator to identify potential retirement income gaps

To use the Wealth Enhancement Retirement Income Calculator, you first need to navigate to the calculator’s page, here. From there, you’ll enter your own personal details, such as your current age, target retirement age, current savings, expected lifestyle costs, and more. The more accurate the information you enter, the more helpful your retirement income projections will be. Remember that Wealth Enhancement keeps all of your information confidential.

After you enter your information, the calculator will project your savings growth and estimate the income you need. Our calculator leverages powerful forecasting algorithms to help you understand how much more you need to save to enable the retirement of your dreams.

Once you’ve fully understood your calculator’s initial output, play around with the inputs and explore different scenarios. For instance, you can see how your retirement income will change if you adjust your target retirement age or your savings rate. This can help you understand the impact of the different decisions you make as you continue on your retirement planning journey.

Use a Retirement Income Calculator to Test Your Plan

If you’re asking questions like “How much do I need to retire?” or “Am I financially ready to retire?” a retirement income calculator can help provide a starting point. It can also help uncover a retirement income gap between your expected income sources and future spending needs.

Next Steps After Using the Calculator

Once you’ve reviewed your retirement income projections, consider taking additional steps such as:

- Reviewing your retirement withdrawal strategy

- Evaluating tax planning opportunities before retirement

- Updating estate planning documents and beneficiaries

- Exploring Medicare and health care planning options

- Assessing business succession or exit strategies

- Meeting with a financial advisor to stress-test your retirement income plan

Planning for retirement doesn’t have to be daunting, but it is a critical aspect of financial wellness. With the Wealth Enhancement Retirement Income Calculator, you can illuminate the path towards a comfortable and secure retirement.

Whether you’re learning how to prepare for retirement in your 50s, evaluating retirement planning for business owners, or building a retirement readiness checklist for high-income earners, having a personalized strategy can make a meaningful difference.

Remember, while this calculator is a powerful planning tool, it’s just the beginning. Everyone’s financial situation is unique, and navigating the complexities of something as complicated as retirement planning can be incredibly challenging. If you have questions about your calculator results, need more information, or want more guidance on your journey to retirement, reach out to a Wealth Enhancement financial advisor today and schedule a complimentary, no-obligation meeting.

Frequently Asked Questions About Retirement Readiness

1. What is retirement readiness?

Retirement readiness refers to your ability to financially support your desired lifestyle in retirement through savings, investments, income planning, and risk management.

2. How do I know if I’m ready to retire?

You may be ready to retire if your projected retirement income can support your expected expenses, health care costs, taxes, and long-term lifestyle goals.

3. How much income do I need in retirement?

The amount varies based on your lifestyle, retirement age, health care needs, travel goals, and inflation assumptions. A retirement income calculator can help estimate your needs.

4. What are the 5 steps to prepare for retirement?

The five key steps include assessing your finances, estimating retirement expenses, choosing a retirement age, planning for inflation and taxes, and testing your plan with a retirement income calculator.

5. What should I do 5 years before retirement?

Focus on retirement income planning, debt reduction, Medicare planning, Social Security strategy, tax planning, and reviewing your investment allocation.

6. When should I claim Social Security?

You can claim benefits as early as age 62, but delaying benefits may increase your monthly income. Your ideal claiming age depends on your financial situation and retirement goals.

7. How does inflation affect retirement planning?

Inflation can reduce purchasing power over time, which may require retirees to adjust spending, investment strategies, and withdrawal plans.

8. Should business owners plan differently for retirement?

Yes. Business owners often need additional planning around succession, liquidity, taxes, and converting business equity into retirement income.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

#2026-12467

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.