Weekly Market Movers | July 13, 2026

Today on Weekly Market Movers:

- Markets largely ignored the renewed tensions with Iran and higher oil prices, showing continued confidence in the economy.

- Early earnings reports suggested higher fuel costs are still affecting both businesses and consumers.

- Global events and AI remained major market drivers—with semiconductor (chip) demand and AI infrastructure spending at the center of earnings growth.

- Bond returns increased as investors lost confidence that interest rate cuts will happen soon.

- Market focus now shifts to earnings, inflation reports, AI developments, and new Fed Chair Kevin Warsh.

Watch the full video:

Chart of the Week

Transcript:

Hello, and welcome to this edition of Weekly Market Movers from Wealth Enhancement. My name is Aya Yoshioka, Director and Senior Investment Strategist. In these videos, we’d like to focus on three things. First, we’ll recap what happened in markets this week. Second, we’ll talk about what drove that performance. And lastly, we’ll look out into the week of July 13 and see what we should all be focusing on.

All right, well, let’s start with looking at year-to-date asset class returns for the week ending July 10.

Well, I want to recap what happened last week, and U.S. stocks were mixed. We started the week off with a resurfacing of geopolitical tensions. It really weighed on markets.

We got a rally, though, on Thursday and Friday, bringing most U.S. indices back into the green. The S&P 500 was up 1.2% for the week, bringing year-to-date gains to 11.4%.

Small caps were unable to recapture or rebound back during the week, and they were down 0.6% for the week, but they’re still up over 20% for the year, as you can see in this chart.

Stocks outside the U.S. were down a little over 1% for the week, with international developed stocks down 1.4% and emerging market stocks down 1.8%. Not too surprising, with Brent crude oil back to $76 per barrel, up about 5% for the week, as hostilities between the U.S. and Iran flared up again.

Still, emerging market stocks have been leading the charge this year and are up nearly 23% on a year-to-date basis.

Fixed income here on a year-to-date basis is flat, and some have said fixed income has been boring. But when you look into the details, you know, we saw U.S. Treasury yields climb higher during the week, and the two-year closed at 4.21%, up seven basis points for the week.

The 10-year yield was also up during the week. It closed at 4.56%, up eight basis points for the week and 10 basis points shy of the 2026 high of 4.6s6.

Well, now that we’ve recapped last week’s market moves, let’s dig into what drove these moves. Since the end of the first quarter of 2026, we’ve been saying that two topics have been influencing market moves the most. First is that geopolitical tension, or the conflict in Iran specifically.

And second is the durability, or the sustainability, of the AI-related trades.

This week was no different. Attacks on commercial ships transiting the Strait of Hormuz began on Monday. And by Wednesday, President Trump was warning that the ceasefire was at risk and it may be over.

This pressured oil prices higher, as I mentioned, and inflation concerns were back in play, lifting Treasury yields higher.

On the AI or tech side of the equation, well, the biggest market move during the week came when the American Depository Receipts, or the ADRs, of Korean memory chipmaker SK Hynix came to the market. The ADR surged 13% above their offering price on Thursday after the chipmaker raised $26.5 billion in the largest-ever U.S. listing for a foreign company.

Thanks to this successful listing, some of the recent concerns that had been weighing on semiconductor and tech stocks in general were alleviated, and tech was once again the best-performing U.S. large-cap sector, up 3.4% for the week.

From a corporate headline standpoint, earnings season officially kicked off with earnings reports from Delta Air Lines and PepsiCo.

Both companies called out that the impact of higher energy prices was lingering.

Delta said that higher fuel costs were keeping airfares elevated, and higher gasoline prices were impacting Pepsi’s Frito-Lay business.

And they stated that consumers were pulling back spending on snacks.

Now, looking out to the week of July 13, we get major banks reporting, companies like JPMorgan, Goldman Sachs, Bank of America, and Citigroup.

And we note that the higher interest rate backdrop that we have, strong loan growth that we’re seeing, and the robust capital markets should all position banks in a positive light, and they should be able to deliver both growth and operating leverage. However, some of these expectations are baked into the current price.

When we look at the S&P 500 in totality, Wall Street is expecting strong earnings growth for the second quarter.

The strength that we saw in the first quarter is expected to continue, with expectations of 22% EPS growth on a year-over-year basis for companies in the S&P 500.

Much of this is tied to the continued growth of the AI infrastructure buildout. And to that effect, Goldman Sachs noted that AI infrastructure stocks account, or are expected to contribute, nearly 60% of that 22% earnings growth.

Micron and Nvidia alone, those two stocks account for more than 40% of that earnings growth. These are big numbers.

Considering, though, that Micron just reported and Nvidia doesn’t report until the end of August, we won’t have too much from those two.

However, because of that, the focus will likely shift to the hyperscalers, companies like Amazon, Microsoft, Alphabet, and Meta.

We’ll also get some additional information from other semiconductor stocks, stocks like Broadcom. And this week, we will hear from Taiwan Semiconductor as they report their monthly June numbers, as well as their second-quarter earnings report.

Now, in addition to all of this earnings information, the week of July 13, we’ll have several economic data releases that will include details on the federal budget balance, retail sales, industrial production, and consumer sentiment.

However, the most watched data will be related to inflation as we get the consumer price index as well as the producer price index during the week.

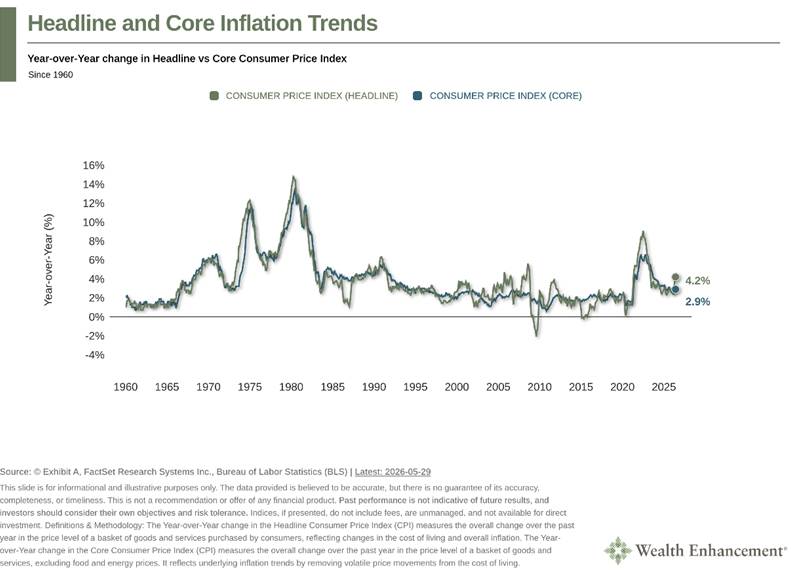

With that, I wanted to share what the charts look like for inflation.

And so, on Tuesday, we get CPI data, and economists are projecting that lower energy prices that we’ve seen over this past month will translate into a year-over-year CPI print of 3.8%, down from last month’s 4.2%.

The print for core CPI, which excludes food and energy, is expected to remain flat from last month’s 2.9%.

Now, the CPI report will be followed by the PPI report, or the Producer Price Index report, and expectations are for a 6.2% year-over-year headline number, down from last month’s 6.5% number seen here.

Again, this is thanks to lower energy prices.

However, core PPI, the number that excludes food and energy, is expected to increase to 5.2% on a year-over-year basis from last month’s 4.9%.

Lastly, the market will get the first semiannual testimony to Congress from the new Fed Chair, Kevin Walsh.

He’ll be in front of the House Financial Committee on Tuesday, and he’ll be in front of the Senate Banking Committee on Wednesday.

And just given his open aversion to forward guidance, he’s unlikely to offer too much in terms of the path forward on interest rates, which is why the inflation data that we get this week will likely carry a lot more weight for markets.

Well, that’s all I have for you this week. Thank you so much for watching our Weekly Market Movers videos from Wealth Enhancement. Thanks again, and we’ll see you next week.

This information is not intended as a recommendation. The opinions are subject to change at any time and no forecasts can be guaranteed. Investment decisions should always be made based on an investor’s specific circumstances. Investing involves risk, including possible loss of principal.

2026-13162

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.