October 2022 Market Commentary

5 minutes

Executive Summary

Despite Federal Reserve action on interest rates and a continued decline in gasoline prices toward pre-Ukraine invasion levels, elevated inflation remains, which prompted further Fed intervention in September. Recession fears and negative market sentiment roiled markets for the month to pave the way for a difficult (and rare) year for both stocks and bonds. While recession risk has elevated, and significant uncertainty persists, investors should refrain from making rash investment timing decisions and remain focused on long-term investment goals.

What Piqued Our Interest

In line with long-term stock market monthly averages, September proved to be a difficult month for investors. Upon review of recent events and market performance, here are some of the major themes driving markets and their implications going forward:

Rate hike(s)

The Federal Reserve raised their federal funds target rate 0.75% on September 21, bringing the target range to 3–3.25%. Rates are expected to be raised an additional 1.25% by year-end, and further increases of 4.75–5% are possible in 2023. The market’s negative reaction to the recent hike raises fears that a recession is becoming increasingly likely.

Inflation

Headline inflation came in slightly lower than the previous month’s readings at 8.3%. While lower gasoline prices helped to moderate the level of growth, persistent supply-chain issues and rising residential rents continue to keep inflation at historic levels.

Energy

Consumers benefited from lowered gas prices through the summer, as the national average for regular gasoline dropped from $4.92 in June to $3.70 by the end of September, according to the U.S. Energy Administration. That relief will likely be short-lived, as OPEC recently announced a significant production cut of 2 million barrels daily. Additionally, upward pressure on natural gas prices here in the U.S. should continue following the destruction of the Nord Stream pipeline in Europe. Combined, those events could provide upward pressure on energy prices and, ultimately, inflation.

Bear market territory

After a disastrous month for equities, both the S&P 500 and MSCI ACWI Indexes are in bear market territory through year-end September at 23.87% and 25.63%, respectively. Regardless of the classification, negative sentiment remains, and recession probability estimates have increased.

There is further downside potential for stocks, as more rate increases loom and higher inflation seems likely for longer. Negative headlines from major companies like FedEx, Nike, and Apple add to slowdown and recession fears. Despite positive job market statistics, Tech sector hiring freezes and layoffs will likely spread elsewhere if the economy continues to slow down further.

Consumer health

Post-Covid, consumer savings rates have dropped toward historic lows. Additionally, outstanding debt has increased, with a greater reliance on installment purchases and credit cards. As the near-term outlook for rates remains less than ideal, a stretched consumer base does not bode well for economic growth.

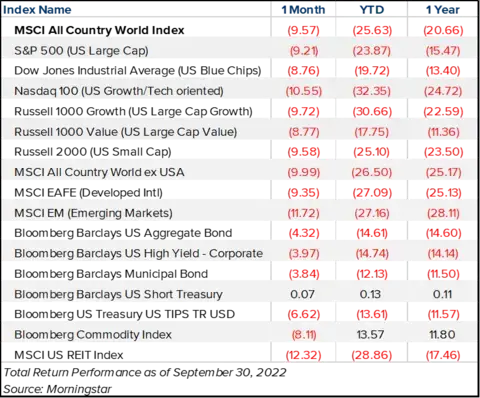

Market Recap

Outside of cash and short-term Treasuries, it was a very difficult month for both stock and bond investors. Equities were down significantly across the board, as the MSCI All Country World Index fell by 9.57%. Continued rate increases weighed more on Growth-oriented stocks than their Value counterparts; year-to-date, the Russell 1000 Value Index is down 17.75% vs. 30.66% for the Russell 1000 Growth Index.

Accordingly, the Nasdaq 100 Index was the worst performer of the major U.S. Indexes at -10.55%. The Small Cap Russell 2000 Index dropped 9.58%, while MSCI EAFE and MSCI Emerging Markets Indexes returned -9.25% and -11.17%, respectively. All three indexes are underperforming the U.S. Large Cap S&P 500 year-to-date. Real estate investment trusts (REITs) continue to struggle through the rising rate environment, posting -12.32% for the month and -28.66% YTD.

The Bloomberg Commodity Index fell in line with stocks with a -8.11% return, driven mainly by falling natural gas and crude oil prices. Despite recent results, Commodities are the best-performing asset class through 2022 at 13.57%.

As expected with rate increases, fixed income also fared poorly, as the U.S. Aggregate Bond Index fell 4.32%. The broad index is now down 14.61% on the year and continues to be on pace for its worst year since its inception in 1976. Municipals continue to modestly outperform taxable bonds, and short-term Treasuries remained flat throughout the year. Despite having inflation protection, inflation-linked bonds (or TIPS) are not immune to interest rate increases. The broad Bloomberg U.S. TIPS Index was down -6.62% and -13.61% for the month and YTD, respectively.

Closing Thoughts

We believe there is an elevated probability of a recession occurring towards the end of this year and into the beginning of 2023. While there is no certainty or consensus as to the timing, duration, or severity of a slowdown, labor market and corporate earnings data suggest it may not be long or severe. It is highly likely (and often mentioned) that continued Fed rate increases will drive the U.S. to recession. One real concern is that the Fed is powerless to tackle inflation under the current scenario, as a significant contributor to recent inflation is excessive government spending—not an overheating economy. As the outstanding National Debt has passed $31 trillion, there appear to be no attempts to rein in spending. Hence, rate hikes will kill economic growth, and stagflation will be a real possibility.

Regardless of predictions or actual outcomes, expectations continue to impact investor sentiment, as recent equity outflows and performance indicate. Often, negative sentiment and resulting investor reactions can overreach, providing ideal entry points for long-term, strategic investors. We consistently advocate against trying to time the market, as rebounds are often quick and unpredictable. We continue to see more attractive valuations across equities and bonds, as stock earnings multiples decrease and bond yields increase to more acceptable levels. Despite elevated recession risks, investing into a diversified portfolio as valuations improve is rational and justifiable for investors with a long time horizon.

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.