Explaining Charitable Lead Trusts

11 minutes

A charitable lead trust (CLT) is a popular gifting technique that combines charitable planning with tax planning. It’s a split-interest trust, meaning the beneficial interests are split between charitable purposes and non-charitable beneficiaries.

CLTs help families support meaningful causes while also reducing their tax burden and preserving wealth for future generations. Below, we’ll break down how CLTs work, the tax advantages they offer, the risks to be aware of, and how to decide if one is right for your goals.

How Charitable Lead Trusts Work?

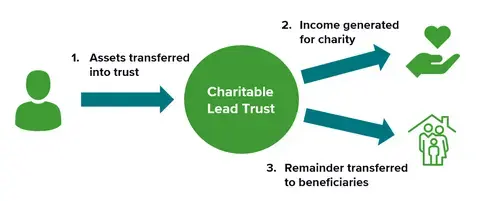

A CLT provides an income stream to a charitable organization, with the remainder going to individual beneficiaries. The income stream is provided for a set number of years, known as the “lead” period, which can be a set number of years or for the life of an individual.

At the end of the lead period, the remainder is distributed to the non-charitable beneficiary (usually one or more loved ones).

A CLT is simply the inverse of a charitable remainder trust (CRT), which provides an income stream to beneficiaries with the remainder going to charity. Unlike CRTs, there is no restriction on how long the CLT can last or on how high or low the payment rate can be.

By using a CLT, a person can provide an income stream to a charity that’s important to them, all while reducing their tax burden and ultimately transferring wealth to their beneficiaries.

Types of Charitable Lead Trusts

There are two main types of CLTs: an annuity trust (CLAT) and a unitrust (CLUT).

A CLAT provides an annuity to the charity that is a fixed sum, set at the inception of the trust. A CLUT provides an annual payment that is equal to a percentage of the annual fair market value of the trust.

Grantor vs. non-grantor CLTs

In addition to deciding between an annuity or unitrust, the trust grantor has to decide whether the trust will be taxed as a grantor trust–meaning all trust income flows through to the grantor’s tax return–or a non-grantor trust–meaning the trust itself is taxed on its income.

The income tax and estate tax deductions that are available to the grantor depend upon whether the CLT is a grantor or non-grantor trust.

When using a grantor CLT, the grantor gets an income tax deduction for the present value of the expected payments to the charity. This can be useful when the grantor expects a year of high income and wants an immediate income tax deduction.

When using a non-grantor CLT, the grantor does not receive an income tax deduction, but does receive a gift tax deduction for the present value of the expected payments to the charity.

Why Use a Charitable Lead Trust?

CLTs are attractive to families who want to blend charitable giving with long-term financial planning. They offer a convenient way to create ongoing support for a charitable organization of your choice, while also removing assets from the taxable estate and reducing the tax burden.

Families often use CLTs to pass appreciating assets, such as stocks or real estate, to their heirs at a lower tax cost than they would otherwise be able to. The better the trust’s investments do, the more value flows to beneficiaries.

For families already planning to make significant charitable gifts, a CLT can help combine that with a powerful tax-advantaged wealth transfer strategy.

Advantages and Disadvantages of a Charitable Lead Trust

CLTs have some key benefits for families who want to transfer wealth in a tax-advantaged way, but also some downsides and risks to consider.

Advantages

- Lower estate and gift tax burden: A CLT can help lower the estate or gift taxes on the assets you transfer to your beneficiaries.

- Income tax deduction: In addition to the estate and gift tax benefit, CLTs may be eligible for an upfront income tax deduction.

- Long-term charitable giving: A CLT helps you create a philanthropic impact through long-term charitable giving.

- Wealth transfer: A CLT helps transfer significant wealth to your loved ones when the charitable term ends, often at a tax-advantaged rate.

- Flexible terms: There are different types of CLTs, meaning each family can choose the terms that work best for them.

Disadvantages

- Irrevocable in nature: CLTs are irrevocable trusts, meaning you can’t change your mind and take the money back later or easily change the beneficiaries.

- Administrative burden: CLTs can be expensive and complex to manage, with ongoing administrative responsibilities and oversight.

- Remaining tax liability: A CLT doesn’t necessarily fully eliminate your tax burden, and the trust could still be required to pay taxes on its earnings.

- Reduced benefit to beneficiaries: The more money you pass along to charitable beneficiaries, the less you’re able to pass along to your loved ones.

- Subject to market volatility: A volatile market could reduce the amount of money that’s passed along to your loved ones in the end.

Who Should Consider a Charitable Lead Trust?

A CLT may be a good option for individuals and families with significant assets who have both charitable giving and estate planning goals. Given the irrevocable nature of CLTs, they’re also only suitable for those who are comfortable tying up their assets in a trust without the ability to access them later.

CLTs are most commonly used by high-net-worth families who want to reduce the size of their taxable estate, while also passing along money to both their favorite charitable organizations and their loved ones.

Considerations Before Establishing a Charitable Lead Trust

Because of the permanent and complex nature of CLTs, careful planning is essential. Here are some of the key considerations when establishing this type of trust:

- Irrevocability: Because CLTs are irrevocable trusts, you should only contribute as much money as you’re comfortable permanently parting with.

- Trust type: There are several different types and tax structures of CLTs, so it’s important to consider which is the best fit for your situation.

- Term length: Some CLTs last for a set number of years, while others last for the remaining lifetime of the grantor.

- Types of assets: The assets you choose can affect the trust’s long-term cash flow and how much you’ll be able to leave to your loved ones.

- Beneficiaries: When establishing the trust, you’ll have to choose both your charitable and non-charitable beneficiaries.

Tax Implications of Charitable Lead Trusts

CLTs have a few different key tax implications. One of the most appealing features of these trusts is the reduction of gift and estate taxes. You’re able to pass along assets to your loved ones without the hefty tax bill.

When the assets are transferred into the trust, the IRS calculates the value of the taxable gift by subtracting the present value of the charitable payments. If the trust performs well, the appreciation passes to your heirs with little additional tax.

The income-tax treatment of CLTs varies between grantor CLTs and non-grantor CLTs. Grantor CLTs provide a tax deduction in the year the trust is created, but the donor has to report all of the trust’s income going forward. Meanwhile, non-grantor trusts have no upfront tax benefit, but the trust itself deducts its charitable payments each year, resulting in tax efficiency.

Capital gains treatment varies depending on the type of trust and the assets contributed. Because there are so many different options and tax characteristics, it’s critical to consult a tax professional when setting up your CLT.

How Market Volatility Affects Charitable Lead Trusts

Market performance plays a significant role in how successful your CLT will be. Charitable payments are made regardless of how the trust performs, but payments to your beneficiaries are dependent on market performance.

As a result, a period of poor returns can reduce the amount eventually left for your heirs. On the other hand, a period of strong market performance can result in a larger payout for your loved ones.

Trustees often manage CLTs with diversified, long-term investment strategies to help strike a balance between growth potential and reliable payouts. It’s important to consider how much risk you’re comfortable with when setting up your trust.

Is a Charitable Lead Trust Right for You?

Whether a CLT is right for you depends on your financial assets, tax burden, and charitable giving goals. You might consider a CLT if you want to make a meaningful charitable impact, while also transferring wealth to your loved ones later on.

It’s best-suited to people who already plan to make significant charitable gifts, as well as those who might otherwise be subject to large estate or gift taxes.

Because CLTs involve complex tax rules and require careful coordination across legal, tax, and investment skillsets, working with a financial advisor well-versed in CLTs is essential. The right professional can help evaluate your potential tax savings, walk you through the various trust structures, and help you decide whether and how a CLT fits with your overall financial goals.

To speak with a financial planner and learn whether a CLT is right for you, set up an appointment with a Wealth Enhancement advisor today.

Frequently Asked Questions about CLTs

What is a charitable lead trust and how does it work in estate planning?

A charitable lead trust (CLT) is an irrevocable trust that splits the benefit of your assets between charity and your chosen non-charitable beneficiaries.

- You transfer assets (such as cash, stocks, or other investments) into the CLT.

- For a set period of years or for a lifetime, the trust pays an income stream to one or more charities.

- When that “lead” period ends, whatever is left in the trust goes to your non-charitable beneficiaries, often children or other family members.

In estate planning, a CLT can reduce estate and gift taxes by removing future appreciation from your taxable estate. You support charities during your lifetime or a set term while still aiming to pass significant wealth to your heirs later, often with a reduced transfer tax cost.

What is the difference between a charitable lead annuity trust (CLAT) and a charitable lead unitrust (CLUT)?

Both are types of CLTs, but they calculate the charity’s payment differently:

Charitable Lead Annuity Trust (CLAT)

- Pays a fixed dollar amount to charity each year.

- The payment does not change, even if the trust value rises or falls.

- Works well when you want predictable payments to charity.

- Pays a fixed percentage of the trust’s value each year.

- The payment is recalculated annually based on the trust’s fair market value.

- If the trust grows, the charity’s payment grows. If the trust declines, the payment drops.

Charitable Lead Unitrust (CLUT)

The choice between CLAT and CLUT usually turns on your desire for fixed versus variable charitable payments and your expectations about investment performance.

How do grantor vs non-grantor charitable lead trusts differ in terms of income, gift, and estate taxes?

The same basic structure can be taxed in two very different ways depending on whether the CLT is a grantor or non-grantor trust.

Grantor CLT

- Income tax:

- The grantor is treated as the owner for income tax purposes.

- The grantor receives a large upfront income tax deduction for the present value of the charity’s interest.

- Ongoing trust income is taxable to the grantor during the trust term.

- Gift and estate tax:

- The grantor makes a taxable gift of the remainder interest to the non-charitable beneficiaries.

- The value of that gift is discounted because of the charitable payments, which can reduce gift and estate tax exposure.

Non-grantor CLT

- Income tax:

- The trust is a separate taxpayer.

- The grantor generally does not receive an income tax deduction when funding the trust.

- The trust deducts the amounts paid to charity each year, which can reduce or eliminate income tax at the trust level.

- Gift and estate tax:

- Like a grantor CLT, the taxable gift is the present value of the remainder interest going to the non-charitable beneficiaries.

- Future appreciation inside the trust can pass to heirs at a reduced transfer tax cost.

Choosing between grantor and non-grantor status is mainly a trade-off between an upfront income tax deduction versus ongoing income tax responsibility and the overall estate planning goals.

What are the main advantages and disadvantages of using a charitable lead trust for my heirs and favorite charities?

Key advantages

- Lower estate and gift tax exposure:

Moving assets into a CLT can reduce the taxable value of your estate and the size of your taxable gift to beneficiaries. - Potential income tax deduction:

With a grantor CLT, you may receive an upfront income tax deduction for the present value of the charity’s lead interest. - Long-term charitable impact:

The CLT funds your preferred charities over many years instead of a single lump-sum gift. - Wealth transfer to loved ones:

After the charitable term, the remaining assets pass to your chosen beneficiaries, often at a more favorable transfer tax cost. - Flexibility of design:

You can choose a CLAT or CLUT structure, set the term length, pick the payout rate, and name both charitable and family beneficiaries.

Key disadvantages

- Irrevocable structure:

Once you place assets into the CLT, you lose direct control and generally cannot pull them back or easily change the beneficiaries. - Administrative complexity and cost:

CLTs require legal setup, ongoing administration, tax filings, and investment management. - Remaining tax exposure:

A CLT may not eliminate all estate, gift, or income taxes; the trust can still owe tax on earnings not paid to charity. - Reduced benefit for heirs during the term:

Because charity receives income first, your family does not benefit until the lead period ends. - Market risk:

Poor market performance can reduce both charitable payments (in a CLUT) and the remainder left for heirs.

Who should consider setting up a charitable lead trust and what asset levels make it worthwhile?

A CLT is typically best suited for:

- Individuals or families with significant wealth who are already inclined to make sizable charitable gifts.

- Those expecting estate or gift tax exposure who want to move appreciating assets out of their taxable estate.

- People comfortable placing assets into an irrevocable structure, knowing they cannot access them later.

- Donors who want to support favorite charities for a period of time and then leave what is left to children or other loved ones.

Because CLTs involve setup costs and ongoing administration, they are most often used by high net worth households rather than small estates. The decision is less about a fixed dollar threshold and more about whether you have enough assets, charitable intent, and tax exposure to justify the structure and complexity.

How are charitable lead trusts taxed and what tax deductions can I receive as the grantor?

Tax treatment depends on the CLT’s structure.

- Income tax

- In a grantor CLT, the grantor can take an upfront income tax deduction for the present value of the charity’s lead interest, subject to normal charitable deduction limits. The trade-off is that all trust income during the term is generally taxable to the grantor.

- In a non-grantor CLT, the trust itself is taxed on its income. The trust deducts the amount paid to charity each year, which can reduce or eliminate the trust’s income tax, but the grantor usually does not receive an initial income tax deduction.

- Gift and estate tax

- When assets are transferred to the CLT, the taxable gift is the present value of the remainder interest that will eventually pass to non-charitable beneficiaries.

- The present value of the charitable payments reduces the gift’s value for transfer tax purposes.

- Any growth in the trust above the IRS assumptions can pass to your heirs with little additional transfer tax.

- Capital gains

- Capital gains treatment depends on trust design and which assets are sold.

- The trust can be structured so that gains are recognized at the trust or grantor level, again depending on grantor vs non-grantor status.

Because tax rules are complex and subject to change, a CLT should be coordinated with your tax, legal, and financial advisors.

How does market volatility affect the payouts from a charitable lead trust to charities and beneficiaries?

Market performance directly influences how a CLT works out for both charity and heirs:

- In a CLUT, charitable payments are a percentage of the trust value. If the market falls, that value drops and charitable payments decline. When the market rises, payments increase.

- In a CLAT, the charity receives a fixed dollar amount each year, so the trust may need to distribute a greater share of its assets in down markets to meet that obligation.

For beneficiaries:

- If investment returns are strong over the trust term, the trust can grow even after making charitable payments. That can leave a larger remainder for your loved ones.

- If returns are weak or negative, the trust may shrink, and the amount available for your heirs at the end of the term can be smaller than initially projected.

Because of this, trustees usually pursue a diversified, long-term investment strategy that balances growth potential against volatility risk in line with your goals and comfort with risk.

What factors should I consider when choosing the term length, assets, and beneficiaries for a charitable lead trust?

Key design choices include:

- Irrevocability and liquidity needs

Only contribute assets you can afford to part with permanently. A CLT is not a source of emergency funds. - Trust type and tax status

Decide whether you want a CLAT or CLUT and whether the trust will be treated as a grantor or non-grantor trust for tax purposes. This affects income taxes, deductions, and administrative work. - Term length

You can choose a fixed number of years or a lifetime term.- Longer terms can increase the charitable impact and potential transfer tax benefits.

- Shorter terms provide quicker access for beneficiaries.

- Assets contributed

Assets that are expected to appreciate, such as stocks or other growth investments, are often attractive for CLTs. You also need to think about:- Liquidity for making annual charitable payments.

- Income generation potential.

- Volatility and how much risk you are comfortable with.

- Beneficiaries

You must name both charitable and non-charitable beneficiaries. Consider:- Which charities align with your values and goals.

- Which family members or other individuals you want to benefit, and how the timing of the remainder payout fits their needs.

- Administrative and professional support

CLTs require legal drafting, tax reporting, and ongoing oversight. You will usually want a corporate or individual trustee with the resources and expertise to manage the trust properly.

How do charitable lead trusts compare to charitable remainder trusts for long-term charitable giving and wealth transfer?

Charitable lead trusts (CLTs) and charitable remainder trusts (CRTs) are opposites in terms of who benefits first:

- Charitable Lead Trust (CLT)

- Charity receives the income stream during the trust term.

- Non-charitable beneficiaries receive what is left at the end of the term.

- Often used to shift appreciating assets to heirs at a reduced transfer tax cost while providing current support to charity.

- Charitable Remainder Trust (CRT)

- Non-charitable beneficiaries (often you or your family) receive income during the term.

- Charity receives what is left at the end of the term.

- Often used for income planning and to diversify appreciated assets while providing a future charitable benefit.

If your priority is immediate, ongoing support to charities with a later transfer to heirs, a CLT may fit better. If your priority is lifetime income to yourself or loved ones with a charitable gift in the future, a CRT may be a closer match. Both are complex and should be evaluated with professional advice to see which structure aligns with your goals.

Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

#2026-10690

Insights

Related resources for you

Get the latest wealth management tips and trends from our library of articles and resources.